-

Introducing Visa A2A

Empowering the future of account-to-account (A2A) payments

A growing demand

A2A payments are rapidly gaining traction in today’s digital economy, becoming essential to the consumer payment experience due to their speed and convenience.

This momentum shows no sign of slowing down.

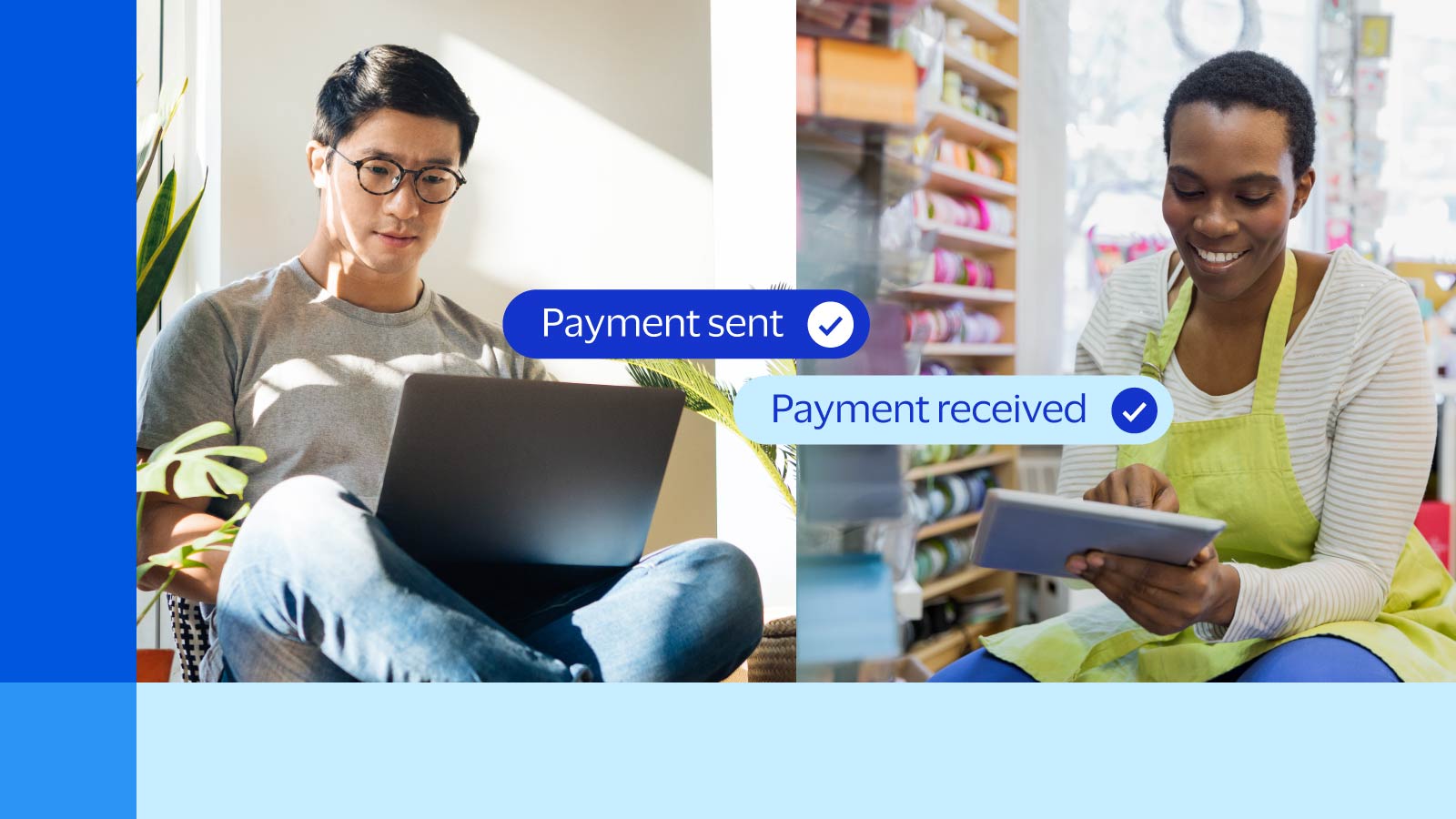

Visa A2A boosts consumer protection with smarter bank transfers

It’s set to transform the ecosystem by integrating Visa's robust capabilities with local payment rails, establishing a trusted network for account-to-account payments.

Visa is leveraging its decades of experience in payment innovation to enhance account-to-account payments with new levels of control and usability.

Core features that empower and elevate

More consumer choice

Greater consumer protection

Standardised user experience

Easy and convenient way to pay

Enhanced control and visibility

Making payments easier for everyday life

Visa A2A is launching soon in the UK, starting with bill payments, soon to be followed by subscriptions. But that’s just the beginning–more use cases are on the horizon, with exciting developments to come.

Bill Pay

Streamline invoicing and recurring payments.

Subscriptions

Manage and customise payments as you need them.

Designed to deliver value for all

Visa A2A for beneficiaries

Visa A2A enhances payment visibility and control, streamlining cash flow management with real-time settlement and comprehensive data for reconciliation. Enabled by Visa, it offers the reliability and adaptability consumers expect and trust.

FAQs

-

-

Existing A2A payments and the open banking landscape at large aren’t providing players with effective dispute management or a sustainable, risk-based commercial model. There also isn’t a singular standard for API and UX, resulting in inconsistent experiences for payers and payees.

Visa A2A integrates Visa's robust capabilities with local payment rails, establishing a trusted network for account-to-account payments. It helps boost consumer protection and control with smarter bank transfers by creating a network of trusted Payer Financial Institutions and Payment Initiators with the ability to initiate A2A payments in a safe and secure way.

-

-

Visa A2A was created in response to the growing global trend in alternative payments—delivering a standard set of rules that governs participants and ensures a fair and consolidated experience.

It builds on the principles of open banking, Variable Recurring Payments (UK) and Dynamic Recurring Payments (EU) by enabling Payers to establish a long-standing consent, with defined parameters, that allows a Payment Initiator to initiate multiple payments over time.

-

-

Payment Initiators and Payer Financial Institutions are participants in Visa A2A and act as service providers to the Beneficiary and Payer respectively.

- Beneficiary Financial Institution: Holds the account on behalf of the beneficiary.

- Beneficiary: Is the seller of goods or services.

- Payment Initiator: Provides technical services to the beneficiary to enable initiation of payments.

- Visa A2A: Operates and manages participation, the rulebook, technical platform for connectivity, and fraud and dispute operations.

- Payer Financial Institution: Holds the account on behalf of the payer.

- Payer: Is the buyer of goods and services.

-

-

Enhanced customer experience and satisfaction: Visa A2A provides customers with increased flexibility and control over recurring payments, which can enhance loyalty and satisfaction.

Secure and reliable A2A payment method: Visa A2A helps ensure transactions are conducted securely and reliably through its robust security infrastructure, offering peace of mind to both banks and customers and bolstering trust.

Faster way to pay: Visa A2A streamlines and standardizes the account-to-account payment experience, offering a flexible, secure and robust solution for modern payment needs across various use cases.

Increased choice and control: Visa A2A helps create more choice for consumers. It’s accessible across banks and TPPs, with consumer-controlled payment conditions that are securely authenticated.

Reliable structure: Visa A2A delivers a central body of rules and standards, ensuring a consistent and reliable experience for Payers.

-

-

Clear economic model: Visa A2A offers an economic model that’s flexible enough to enable different use cases and enables investment and innovation.

Simple connectivity model: Visa A2A enables Payer Financial Institutions to seamlessly connect with Payment Initiators via a single integration with Visa A2A APIs.

Fraud monitoring and reporting: Visa A2A enables fraud monitoring and reporting to help mitigate fraudulent activity.

Robust dispute resolution: Visa A2A offers a clear and robust dispute resolution mechanism to manage disputes.

-

-

Greater customer reach: Payment Initiators will be able to access all participating Payer Financial Institutions and use cases via a unified integration, streamlining operations and increasing access to customer accounts.

Sustainable Commercial Model: Under Visa A2A, Payment Initiators will be able to have a contract directly with Visa to access multiple Payer Financial Institutions across different use cases.

Simple connectivity model: Visa A2A enables Payment Initiators to seamlessly connect with all Payer Financial Institutions via a single integration with Visa A2A APIs.

Fraud monitoring and reporting: Visa A2A enables fraud monitoring and reporting to mitigate fraudulent activity.

Robust dispute resolution: Visa A2A offers a clear dispute resolution mechanism to manage disputes.

-

-

Dispute Resolution Assurance: Visa A2A offers robust dispute resolution management.

Increased security and reduced fraud: Thanks to Visa A2A protections, there’s less opportunity for fraudsters to intercept or steal funds.

Faster, more convenient payments: Visa A2A enables instant or near-instant payments and a seamless way to create mandates for recurring payments, resulting in fewer failed transactions and making it easier for beneficiaries to manage cash flow and reconcile.

Sustainable: Visa A2A is designed to evolve alongside advancements in the payment industry, ensuring Beneficiaries stay relevant and offer consumers the most up-to-date payment options.

Trusted by customers: Customers can use a secure payment method from a brand that they know and trust.

Offer customers flexibility: Give customers flexibility and control over their payments.